Why STP underwriting matters in 2026

STP underwriting - straight-through underwriting - is the practice of letting clean, low-complexity submissions move from quote to bind without a human underwriter touching the file. In 2026 it is no longer a personal-lines novelty. It is becoming table stakes for small commercial and a real differentiator in mid-market and specialty.

I have spent the last twenty years on the carrier side - operations, underwriting, transformation. In my experience working with CUOs, the conversation about STP underwriting always starts the same way. The Chief Underwriting Officer says: "Our combined ratio is fine. The problem is we are losing the simple business to faster carriers, and our senior underwriters are spending 40% of their time on submissions a junior could approve in their sleep."

That is the gap STP closes. Not "AI replacing underwriters" (a question I've addressed at length in a separate piece on AI augmentation in underwriting). Codifying the easy decisions so the senior bench has bandwidth for the hard ones.

A few numbers worth holding in mind. According to McKinsey, up to 95% of personal lines policies at leading P&C carriers can move through STP with no underwriter involvement, and 90% of pricing and underwriting tasks for individual and small business policies are projected to be fully automated by 2030.[1] Top-quartile commercial P&C carriers run loss ratios six percentage points lower than peers, with 60% of that performance gap explained by how they operate, not what lines they write.[2] That "how" is overwhelmingly about underwriting discipline plus decision speed. STP underwriting touches both at the same time.

This article is for CUOs and underwriting transformation leads at U.S. P&C carriers and MGAs. It assumes you already have a workbench (or are choosing one) and you are asking the next question: what should actually go through STP, what stays with a human, and how do you prove to your regulator that the line between the two is defensible?

What straight-through underwriting actually means (and what it doesn't)

Straight-through underwriting is end-to-end automation of a quote-to-bind decision: the submission arrives, the system enriches it with third-party data, applies eligibility and pricing rules, scores the risk, and either binds the policy or routes it to an underwriter - all without a human in the loop on the binds. The underwriter only sees the exceptions.

That is the textbook definition. The operational definition matters more.

STP underwriting in P&C: a working definition

For carrier purposes, I treat STP as a decision that meets four conditions:

(1) submission data is structured and validated programmatically,

(2) all eligibility and pricing rules return a clean answer with no manual override required,

(3) the risk score falls inside a pre-approved confidence band, and

(4) the audit trail captures every input, every rule fired, and every decision boundary.

If any one of those fails, it is not STP. It is partially-automated underwriting routed for review - which is also valuable, but a different KPI. (For the broader workbench context that wraps STP, see our 2026 guide to the underwriting workbench.)

What STP underwriting is not

Three things STP is not. It is not "AI underwrites the policy." STP is rules + data + scoring + audit; AI may sit in the scoring layer, but the decision logic is explicit and reviewable. It is not "replace the underwriter." Senior underwriters set and tune the rules, review exception patterns, and own the override decisions - the mix changes, the role does not disappear. And it is not a free pass on regulation. STP decisions are still subject to the NAIC Model Bulletin on AI, state DOI examinations, and Unfair Trade Practices Act review. I'll come back to that in Section 9.

Why the distinction matters for CUOs

When the board asks "what's our STP rate?", a clean answer requires you to define which risks were eligible for STP and which actually cleared the guardrails. I've worked with a Northeast specialty carrier whose CUO told the board they were at 62% STP. We pulled the data: eligible submissions were 71%, cleared submissions were 44%, and 18% of "STP-bound" policies were actually being touched by an underwriter for a quick sanity check that nobody was logging. The real STP rate was 26%. The board needed to know that, and so did the regulator.

The decision-time problem - why simple risks still take four days

I have walked through enough underwriting floors to know the pattern. A clean BOP submission arrives Monday morning. By Thursday afternoon it is bound. Three and a half days. The underwriter's actual hands-on-keyboard time? Forty-seven minutes.

The other three days are not "underwriting." They are queue time, data lookup time, re-keying time, waiting-on-loss-runs time, and the inevitable email thread with the agent because the ACORD form had a missing field.

Where the time actually goes

When I have measured submission cycles directly with carriers - clock running from receipt to bind - the breakdown for a clean small commercial risk usually looks like this. Submission triage and intake: 20–30% of elapsed time. External data lookup (loss runs, MVR, Dun & Bradstreet, ISO scores): 25–35%. Rule application and pricing: 5–10%. Underwriter review and judgment: 10–15%. Quote issuance and binding admin: 15–20%. The decision itself - the actual underwriting - is the smallest slice.

That is the case for STP. You are not trying to replace the underwriter's judgment on the 47 minutes of real work. You are trying to remove the three days of administrative drag that surrounds it.

The competitive cost of latency

In commercial lines, the carrier that quotes in two hours wins more business than the carrier that quotes in two days, even at slightly higher prices. McKinsey's commercial P&C work documents quote-to-issue cycles compressing from days to one or two hours at carriers that have invested in STP plumbing.[3] J.D. Power's 2025 Small Commercial Insurance Study found that ease of doing business is now one of the top drivers of retention, and that satisfaction is identical between customers whose premiums went up and those whose premiums did not - provided the carrier communicated clearly and quickly.[4] Speed is not a "nice to have." It is bound directly to retention economics.

The senior underwriter cost

There is a second cost that does not show up in the cycle-time metric. Every clean BOP your senior underwriter touches is a complex specialty submission they did not have time to think hard about. I have seen carriers run their best underwriters at 60–70% utilization on simple risks the rules engine could have cleared. The opportunity cost is not the cycle-time - it is the loss-ratio impact on the harder book that did not get the attention it deserved.

STP underwriting architecture - quote to bind in seconds

The architecture is straightforward in principle and surprisingly hard to get right in practice. There are five layers, and a weakness in any one of them collapses the whole thing.

Layer 1: Structured submission intake

This is where most STP programs die. ACORD forms arrive as PDFs with hand-typed fields. Loss runs come as scanned spreadsheets. Schedules of values are emails with attachments. If your intake layer cannot turn that mess into structured, validated data without a human, the rest of the architecture is theoretical. I'd require a 95%+ extraction accuracy benchmark on your intake layer before you commit to an STP target. Anything less and you are inventing manual work downstream.

Layer 2: Third-party data enrichment

The submission comes in thin. The decision needs it thick. ISO loss costs, CLUE reports, MVR pulls, Dun & Bradstreet financials, geocoded peril data, and increasingly telematics or IoT signals - all of it has to be pulled, normalized, and attached to the quote in real time. The hard part is not the integrations. It is graceful degradation: what does the system do when the D&B call times out at 3:47 p.m. on a Friday? The answer cannot be "stop." It has to be "score with the data we have, flag the gap in the audit trail, and route if the confidence band drops below threshold."

Layer 3: Rules engine - the explicit logic layer

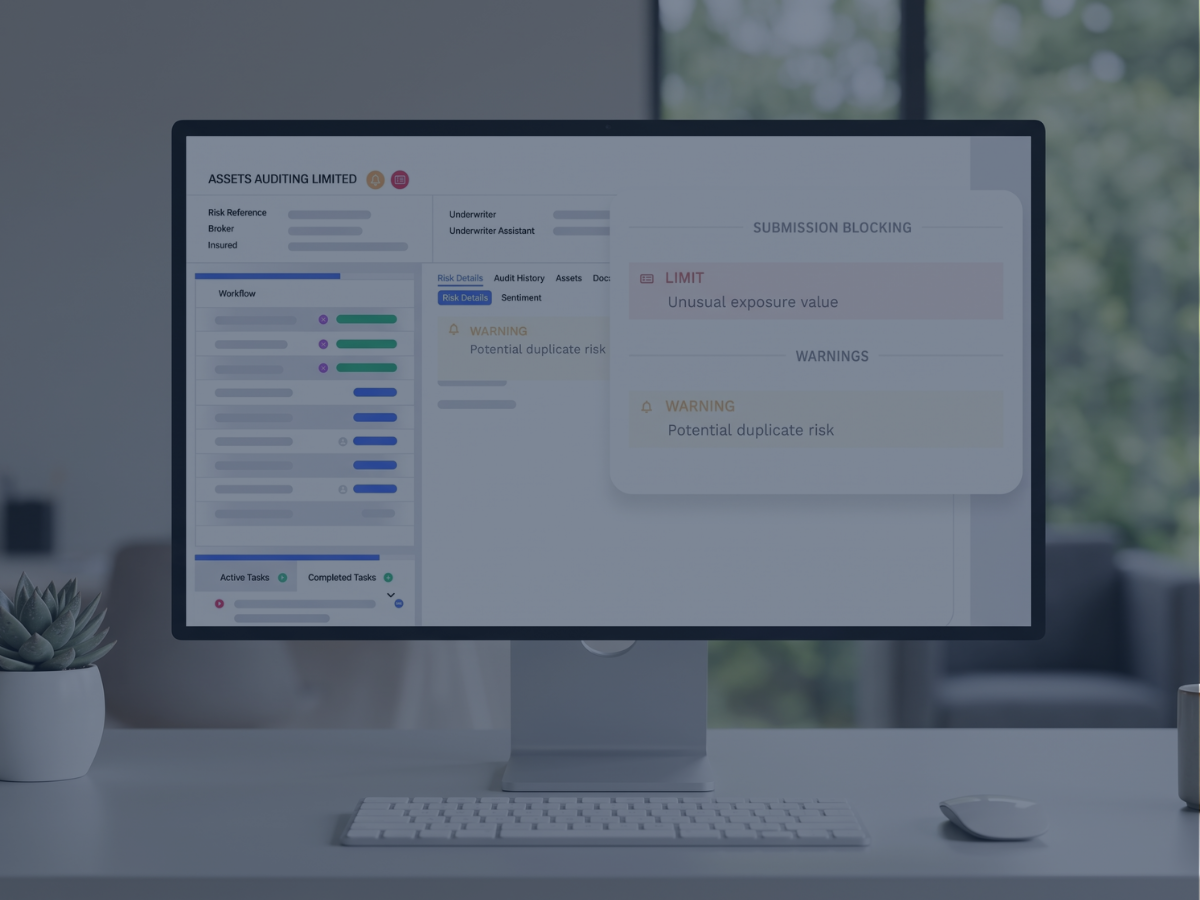

Eligibility, declination, pricing tier, coverage limits, and territorial restrictions are all explicit rules. An insurance business rules engine such as Higson is purpose-built for this layer: business users (not IT) author and version rules, every rule firing is logged, and changes deploy in hours rather than the four-month IT backlog I keep hearing about. The point of an explicit rules layer is auditability. When the regulator asks why a Maryland small auto risk was declined, you should be able to answer in two clicks. (I cover the rules engine layer in more depth in the underwriting rules engine guide in this series.)

Layer 4: AI risk scoring (with confidence bands)

Above the rules layer sits a predictive model. It scores expected loss against the actuarial baseline and produces a confidence interval. The STP decision logic does not say "AI says approve, so approve." It says: "Rules cleared the eligibility gate, AI score is in the green band with confidence above 85%, no fraud signals fired - bind the policy." Confidence bands are how you keep the human in the loop on the cases that need a human. A risk with a 60% confidence band gets routed to an underwriter, with the model's reasoning attached for review. The mechanics of the scoring model itself I cover in more depth in the AI risk scoring piece in this series.

Layer 5: Audit trail and decision logging

Every input, every rule that fired, every score, every override gets logged with timestamp and user identity. This is not a nice-to-have. The NAIC Model Bulletin and the AI Systems Evaluation Tool the NAIC piloted in early 2026 are explicitly designed to inspect this layer.[5] A carrier that cannot produce a defensible decision history per policy is going to fail a market conduct exam in a bulletin state.

How to define a "simple risk" - the eligibility matrix

This is the conversation I keep having with CUOs: "We want to do STP, but every risk is special." No, they are not. Most of them follow patterns. The work is to write those patterns down.

The four-axis eligibility matrix

I recommend defining STP eligibility on four axes: line of business, premium band, loss complexity, and exposure profile. A risk has to be green on all four to be STP-eligible. Yellow on any one routes it to an underwriter. Red on any axis is an automatic decline or refer.

Per-line examples

For small commercial BOP, an STP-eligible risk in my book looks like: premium under $25,000, single-location, standard ISO classification, no losses in last three years, no special exposures (asbestos, swimming pool, dog breed restrictions, etc.), business in operation more than three years, building under 50,000 sq ft. That gets you maybe 50–60% of the BOP submission stream as STP-eligible. The remaining 40–50% routes to an underwriter, which is exactly where you want the senior bench focused.

For personal auto, the matrix is wider - STP rates of 80–90% are achievable. For workers' comp, STP-eligibility narrows sharply: I'd start with monoline, single-state, sub-$50,000 premium, single-class-code risks with three years of clean loss runs.

Eligibility matrix at a glance

The matrix is a starting point. Everycarrier I have worked with has tightened or loosened one of those columns basedon their own loss experience. The point is that the matrix is written down,versioned, and visible to the actuarial team, the underwritingteam, and the regulator.

What I'd require before going live

Before any rule set goes live in STP, in my experience three things make or break the deployment: (1) backtest the rule on at least 18 months of historical submissions, (2) run a one-month shadow mode where the rule fires but a human still binds, comparing decisions, and (3) document the senior underwriter sign-off on the final ruleset. Skipping any of those three is how you end up with adverse selection in the book six months later and no clean rollback path

Rule guardrails - when STP fires, when it escalates

The rules engine is the trip wire. Get the trip wires right and your senior underwriters spend their time on the cases that actually need them. Get them wrong and you either bind risks you shouldn't (adverse selection) or refer cases you didn't need to (defeating the point of STP).

The guardrail hierarchy

I think of guardrails in three tiers. Hard stops are absolute. They override every other signal. Examples: applicant is on a sanctions list, building is in an excluded ZIP code, classification is not on the carrier's appetite. These are non-negotiable and route to decline, not to a human.

Soft stops are confidence-based. The risk passes eligibility, but the AI score sits in the yellow band, or a third-party data signal disagrees with the application data. These route to a human underwriter with the conflict flagged. The underwriter does not start from scratch - they see "model says X, application says Y, here is the discrepancy." That is human-in-the-loop done right.

Override-with-reason rules let underwriters bind risks the rules engine declined, but only with a logged reason code. Over time, the override pattern data is gold. If your underwriters are systematically overriding rule 47, the rule is wrong and needs revision.

Pricing guardrails

Pricing rules need the same treatment as eligibility rules. STP decisions can include a price band: the system binds if the premium falls within a pre-approved range. Outside that range - say, the rules engine wants to charge 18% above the standard rate because of a peril multiplier - the case escalates. This is how you protect against pricing model errors making it into the bound book at scale.

Capacity and aggregation guardrails

Less obvious but equally important: STP cannot be allowed to bind risks that breach portfolio aggregation limits. If you are at 95% of your appetite on coastal property in Florida, the next coastal property submission cannot STP-bind, no matter how clean it looks individually. The guardrail layer needs real-time portfolio visibility - which is why STP architecture and portfolio monitoring are joined at the hip. (More on that in our piece on workbench architecture.)

What good looks like

A well-tuned guardrail layer, in my experience working with CUOs who run STP at scale, produces three signals at the senior underwriter level. First, the volume of cases routed for review is steady or declining as rules mature. Second, the override rate on routed cases is in the 5–15% range - high enough to indicate the routing is meaningful, low enough to indicate the rules are mostly right. Third, the loss ratio on STP-bound business is at or below the loss ratio on underwriter-bound business in the same line. If STP-bound business runs hotter, your guardrails are too loose.

Target STP rates by line - what good looks like in 2026

There is no universal STP rate. The right target depends on line, segment, distribution channel, and risk appetite. The numbers below are the ranges I have seen in well-run programs as of 2026. They are starting points for setting your own target - not benchmarks to chase blindly.

STP target rates by line

Why the ranges vary

Personal auto has decades of standardized data, deep telematics, and small-dollar exposures that tolerate model error. Specialty E&S has heterogeneous risks, long-tail exposures, and individually large premium dollars where a model misfire is expensive. The economics of STP are different on each end of that spectrum.

For mid-market commercial, the right framing is usually not "what STP rate are we hitting" but "what percentage of submissions are we triaging in under 30 minutes, with the underwriter starting from a pre-built case file." That is a better operating metric for the segment.

Setting the right target for your book

In my experience, carriers that pick an STP target without first measuring their submission complexity distribution end up disappointed. The right sequence is: (1) map your last 12 months of submissions across the four-axis eligibility matrix, (2) calculate what percentage could go STP if rules were perfect, (3) set a realistic target at 60–70% of that ceiling, and (4) instrument the gap so you can see why eligible submissions are not clearing - usually the answer is intake data quality, not the rules themselves. The intake-quality conversation is where the Decerto Underwriting Workbench earns its keep - structured ACORD ingestion, third-party data orchestration, and the audit substrate underneath.

Where the ROI shows up

The ROI on STP underwriting is not a single line item. I've seen it land in four places: (1) loss ratio improvement of 3–5 points within 12–18 months from better risk selection consistency, (2) underwriter capacity gains of 2–3x on policies-per-FTE, (3) quote-to-bind ratio improvement of 30–50% from speed, and (4) expense ratio reduction of roughly 10–15% from reduced manual handling. Carriers that set realistic STP targets hit those numbers. Carriers that chase 80% in commercial usually do not.

Three common STP failures (and how to design around them)

I have seen STP underwriting programs fail in roughly the same three ways. None of them are technology failures. All of them are design failures.

Failure pattern 1: the rules library that nobody owns

A carrier rolls out STP, defines 200+ rules across eligibility, pricing, and routing. Six months later, nobody can remember why rule #147 declines applicants over age 75 in Pennsylvania. The actuary who wrote it has rotated to a different role. The compliance team needs to defend the rule to a state DOI. The senior underwriter says "I think we did that because of a 2023 loss pattern, but I'd have to check."

The fix is rule governance from day one. Every rule needs an owner (a named person), a rationale (a written paragraph), an evidence link (the data or the loss event that justifies it), and a review date (every rule expires and gets renewed, or it dies). I'd require this at deployment, not as a documentation task at the end. Deferring it always means it does not happen.

Failure pattern 2: chasing the STP rate, not the loss ratio

A CUO sets an aggressive STP target - say, 60% on small commercial. The team meets it. Loss ratio on the STP-bound book is 5 points worse than the underwriter-bound book at month 12. The carrier looks at the spread and concludes "STP doesn't work for us."

It's not that STP doesn't work. The team optimized for the wrong KPI. STP rate is a process metric. Loss ratio is the outcome metric. I've worked with a Mid-Atlantic carrier whose CUO reframed it as "STP-eligible loss ratio plus or minus 1 point of underwriter-bound loss ratio." That dual constraint forced the team to tighten guardrails when the spread widened, instead of pushing volume through the gate. The STP rate ended up 8 points lower than the original target - and the combined book ran 2 points better in loss ratio. That is the right trade.

Failure pattern 3: the audit trail nobody read

I will keep saying this because it keeps happening. A carrier deploys STP, generates millions of automated decisions over 18 months, then a Texas DOI examiner asks for a sample of 50 declined auto applications with full decision traceability. The carrier discovers the audit logs were structured for engineering debugging, not regulatory review. Reconstruction takes three weeks. The exam goes badly.

The fix is to design the audit trail for the regulator, not for the engineer. Every automated decision needs to be reproducible: same inputs, same rules version, same data snapshots - same output. A regulator should be able to ask "show me this declined application" and get a one-page report with submission data, rules fired, scores produced, decision rendered, all with timestamps. If your audit layer cannot produce that report on demand, you do not have an audit trail. You have logs.

What these failures have in common

All three failures are about discipline, not technology. The technology has been mature enough for STP underwriting for years. What carriers underestimate is the operating model around the technology - rule governance, KPI selection, audit design. I'd rather see a carrier deploy STP on 30% of small commercial with airtight discipline than 60% with the discipline deferred. The first program scales. The second one gets unwound after the first market conduct exam.

NAIC AI Bulletin and STP compliance considerations

STP underwriting decisions are AI-assisted decisions in the NAIC's framing, even when the AI is just a scoring layer above an explicit rules engine. As of August 2025, twenty-four U.S. jurisdictions and the District of Columbia had adopted the NAIC Model Bulletin on the Use of Artificial Intelligence Systems by Insurers in full or substantially similar form, with several more pending.[6] The NAIC Big Data and AI Working Group piloted the AI Systems Evaluation Tool in January 2026, designed to operationalize examiner inquiries into AI governance.[7] Carriers operating STP programs in 2026 should plan for examiner questions, not theoretical compliance.

What the bulletin actually requires

The bulletin is principle-based, not prescriptive. It asks carriers to maintain a written AI Systems (AIS) Program covering governance (named accountability across underwriting, actuarial, data science, legal, compliance), risk management (validation, testing, retesting, bias detection), and third-party vendor oversight. It does not specify a testing methodology or a documentation template. That sounds permissive. It is not. Two carriers can both be "compliant" with very different evidentiary records, and the carrier with thinner evidence will spend more time in examination.

State-level layers above the bulletin

Several states have moved beyond the bulletin. Colorado's algorithm and external data regulations under SB21-169 took effect for life insurance in November 2023 and extended to private passenger auto and health benefit plans on October 15, 2025, with quantitative disparate impact testing requirements that go further than the model bulletin.[8] New York's DFS circular letter on AI in pricing and underwriting expects carriers to demonstrate that external consumer data and AI systems do not produce unfairly discriminatory outcomes, with documented testing and ongoing monitoring. California has imposed restrictions on the sole use of automated tools in health-related decisions, with required clinician review for adverse determinations. If you are a multi-state carrier, the operating standard is not the NAIC floor - it is the most restrictive jurisdiction in your footprint.

What this means for STP design

Three practical implications. First, every STP rule and every model feature needs a documented business rationale and a fairness review. Proxy variables that correlate with protected classes are now examiner red flags. Second, your model card needs to include input features, output, training data lineage, validation results, and known limitations - and it needs to be available in days, not weeks, when requested. Third, your override and exception logs need to be analyzable for disparate impact patterns, not just operational efficiency.

The cross-link to compliance

I have written about this in more depth in the compliance-focused piece in this series (How an Underwriting Workbench Strengthens Regulatory Compliance). For STP underwriting specifically, the takeaway is this: the bulletin is not a tax on STP - it is a discipline that, applied early, makes the program defensible. Carriers that bake compliance into the rule governance from day one have a much easier time at exam than carriers that bolt it on after the fact.

FAQ

What is straight-through underwriting in U.S. P&C insurance carriers?

Straight-through underwriting (STP) is end-to-end automation of the quote-to-bind decision for low-complexity P&C risks. The submission is intaken, enriched with third-party data, evaluated by a rules engine and risk scoring model, and either bound or routed to an underwriter - all without manual handling on the bound cases. STP is most common in personal auto and small commercial BOP, and rare in specialty or large commercial.

How is STP underwriting different from traditional underwriting workflows?

Traditional underwriting routes every submission to a human, who applies judgment supported by tools. STP routes only the cases that need judgment, and binds the rest using explicit rules and validated models. The underwriter's role shifts from processing volume to designing rules, reviewing exceptions, and handling complex risks. The judgment does not disappear - it concentrates where it has the most value.

What STP rate should a P&C carrier target in 2026?

It depends on the line. Realistic ranges are 75–85% for personal auto, 60–75% for personal property, 40–55% for small commercial BOP, and 25–40% for monoline workers' comp. Mid-market commercial typically targets 5–15%. Setting the target requires first measuring submission complexity in your book, then aiming at 60–70% of the theoretical ceiling for that line.

How does an underwriting workbench enable STP underwriting?

A workbench provides the unified interface, data integrations, rules engine, and audit trail that STP requires as plumbing. Without a workbench, you are stitching together intake, enrichment, rules, scoring, and logging across multiple disconnected systems - which is where most STP programs fail. The workbench is not the STP itself; it is the substrate that makes STP operationally sustainable.

Does NAIC AI Bulletin compliance limit what carriers can automate in underwriting?

No, it does not limit what you can automate. It requires that you document and govern how you automate. Eligibility rules, pricing logic, and AI scoring are all permitted under the bulletin and the state-level frameworks above it, provided you maintain the AI Systems Program, run fairness and bias testing, document decisions, and respond to examiner inquiries. Carriers that get governance right preserve full automation flexibility.

What KPIs should a CUO track to measure STP underwriting success?

Track at least four metrics together: STP rate (process), loss ratio on STP-bound business vs. underwriter-bound business in the same line (outcome), quote-to-bind cycle time (customer-facing speed), and underwriter override rate on routed cases (rule quality signal). Tracking STP rate alone leads to chasing volume at the cost of selection quality. The dual constraint of rate plus loss ratio is what keeps the program disciplined.

How long does it take to deploy an STP underwriting program?

Plan for 6–12 months for a first-line deployment if you already have a workbench in place, or 12–18 months if you are deploying the workbench and STP together. The technology is the shorter part. The longer parts are rule extraction from senior underwriters, backtesting on historical submissions, the shadow-mode period before going live, and the rule governance documentation. Trying to compress those steps is how STP programs fail at month 18.

Talk to Decerto / Higson

Every month an STP program is delayed is a month of senior underwriter capacity spent on simple risks, three to five points of loss ratio improvement not realized, and one more month closer to a NAIC AI Systems evaluation in your state. The carriers that move now will write the next decade's rules. The ones that wait will defend the rules other carriers wrote.

What you get with a 30-minute portfolio assessment with my team. We walk through your last 12 months of submissions across the four-axis STP eligibility matrix, identify the realistic STP ceiling for your top three lines, and show you where the rule library would deliver the fastest loss-ratio impact. The conversation is technical, not a sales pitch. You will be on a call with me and a senior architect from the team. NDA-protected, your data stays your data, no commitment past the call.

I'll bring with me a free Higson rules engine sandbox - define one of your real underwriting rules, see it run in tester mode against historical submissions in your portfolio, and see the rule firing pattern and override candidates in real time. That is more useful than any demo deck I can build.

Sources

- McKinsey & Company, The future of AI for the insurance industry (2025) and How data and analytics are redefining excellence in P&C underwriting. McKinsey research indicates that up to 95% of personal-lines policies at leading carriers can move through STP, and that 90%+ of pricing and underwriting tasks for individual and small business policies will be largely automated by 2030.

- McKinsey & Company, Global Insurance Report 2025. Top-quartile commercial P&C carriers run loss ratios 6 percentage points lower than peers, with 60% of the performance gap explained by operating excellence.

- McKinsey & Company, AI in insurance: Understanding the implications for investors (2026). Commercial and specialty P&C models with predictive win rates now deliver quotes in 1–2 hours rather than 2–3 days.

- J.D. Power, 2025 U.S. Small Commercial Insurance Study. Customer satisfaction is identical between customers whose premiums increased and those with no increase, provided the carrier communicated the reason clearly.

- NAIC, Big Data and Artificial Intelligence (H) Working Group - AI Systems Evaluation Tool development and pilot timeline (2025–2026).

- NAIC, Implementation of NAIC Model Bulletin: Use of Artificial Intelligence Systems by Insurers - adopting jurisdictions tracker (updated through 2025–2026).

- NAIC, Model Bulletin on the Use of Artificial Intelligence Systems by Insurers (adopted December 2023).

- Colorado Division of Insurance, C.R.S. §10-3-1104.9 (SB21-169) - algorithm and external data regulations, life insurance (effective November 2023), private passenger auto and health benefit plans (effective October 15, 2025).

- NAIC, P&C AI/ML Survey results - 88% of auto insurers and 70% of homeowners insurers reported using or planning to use AI/ML models in their operations.

- McKinsey-LIMRA, 2025 Insurance 360 Benchmark. 90% of carriers expect to meaningfully increase AI investment over the next two years.

Subscribe to receive the latest blog posts to your inbox every week.