At the heart of every insurance transaction lies a fundamental question: What is the right price for this specific risk? The answer determines profitability, market competitiveness, and customer satisfaction. For decades, the process of finding that answer has been a complex, often cumbersome task. But in today's fast-paced digital landscape, the technology that powers pricing - the insurance rating engine - has evolved from a simple back-office calculator into a strategic asset that can make or break an insurer's success.

Many carriers, however, find themselves constrained by outdated rating methods, unable to adapt quickly to market changes or launch innovative products. This guide is designed to be the definitive resource for 2025, covering everything you need to know about the modern insurance rating engine. We’ll explore what it is, why traditional approaches are no longer viable, and how leveraging a modern engine can drive profitability and a sustainable competitive advantage.

What Is an Insurance Rating Engine?

In the simplest terms, an insurance rating engine is a highly sophisticated calculation tool that determines the premium for an insurance policy. Think of it as the powerful brain behind every quote. While a customer or agent provides a set of inputs - like a driver's age and vehicle type for auto insurance, or a building's construction and location for property insurance - the rating engine processes this information through a complex web of rules, formulas, and data tables to produce a final price.

This process involves:

- Applying Base Rates: Starting with a foundational price for a standard level of risk.

- Executing Rules and Logic: Factoring in dozens or even hundreds of variables (e.g., driving record, credit score, claims history, telematics data).

- Adjusting for Factors: Applying discounts (safe driver, multi-policy), surcharges (lapses in coverage, accidents), and other adjustments.

- Adding Taxes and Fees: Calculating and appending all state-mandated taxes and administrative fees.

In essence, a modern insurance rating engine is a system that translates a unique risk profile into a precise, defensible, and marketable premium in real-time.

The Problem with Traditional Rating

For years, insurers have relied on two primary methods for rating: complex spreadsheets and logic hard-coded directly into their core systems. While functional in a slower-moving era, today these approaches represent a significant bottleneck to growth and innovation.

1. The Spreadsheet Nightmare: Many companies still manage their rates in massive, interconnected Excel files. This practice is fraught with risk. Spreadsheets lack robust version control, leading to confusion over which "Final_v3_Johns_Edits.xlsx" is the correct one. They are notoriously prone to human error - a single broken formula or incorrect cell reference can lead to millions of dollars in misquoted premiums. Furthermore, they offer no security and no clear audit trail, making compliance a constant struggle.

2. The Hard-Coded Prison: The alternative - embedding rating logic directly into a monolithic Policy Administration System (PAS) - creates a different set of problems. In this model, every single rate change, no matter how small, requires a code change, testing, and a full development cycle. This creates a crippling dependency on IT resources. A simple request from the business to adjust a discount factor can turn into a six-month project, effectively stifling the insurer's ability to react to the market. This approach builds significant technical debt, making the entire system more brittle and expensive to maintain over time.

Core Benefits of a Centralized Rating Engine

A modern, centralized insurance rating engine addresses these challenges directly, transforming rating from a liability into a strategic advantage.

- Accuracy & Consistency: A centralized engine acts as the single source of truth for pricing. This guarantees that the quote a customer receives on your website is identical to the one offered by an agent or through a mobile app. This omnichannel consistency is crucial for building customer trust and preventing channel conflict.

- Speed & Agility: This is arguably the most significant business benefit. When your rating logic is decoupled from your core systems, you can update rates, launch new products, or introduce new rating factors in days or weeks, not months or years. This allows you to respond swiftly to competitor moves, react to new regulatory mandates, or leverage new data insights (like from telematics or IoT devices) to gain a first-mover advantage.

- Compliance & Auditability: State regulators demand clear documentation and transparency. A modern rating engine provides a complete, time-stamped audit trail of every change - who made it, what was changed, and when it became effective. Features like versioning and "as-of" rating allow you to perfectly reconstruct any past quote, ensuring you can always demonstrate compliance.

- Scalability: The demands of digital distribution channels are immense. A direct-to-consumer website or a connection to insurance aggregators can generate thousands or even millions of quote requests per day. Legacy systems were not built for this load and will often buckle under the pressure, resulting in slow performance and lost business. A modern, cloud-native rating engine is designed to scale elastically, handling massive volumes without compromising speed.

Key Features of a Modern Rating Engine

When evaluating an insurance rating engine, look for these critical capabilities:

- Complex Rule & Formula Support: The engine must be able to handle sophisticated logic beyond simple arithmetic, including complex nested formulas, matrix lookups, and interdependent rules.

- "What-If" Scenario Testing: This is a crucial feature for actuaries and product managers. It provides a sandbox environment where they can model the impact of potential rate changes across the entire book of business before deploying them to production.

- Versioning and Effective Dating: The system must be able to maintain multiple versions of rates simultaneously and apply the correct version based on a policy's effective date, not the date the quote is run.

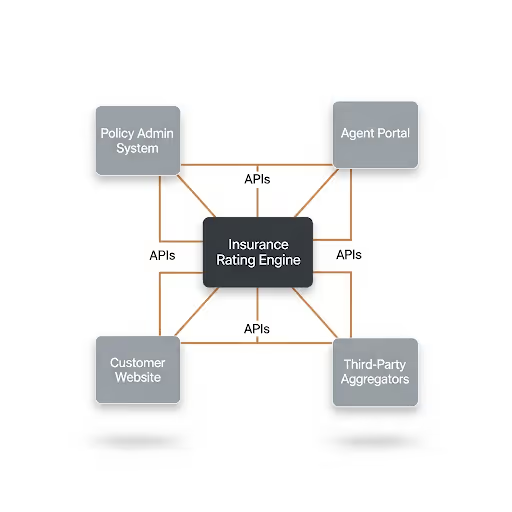

- API-First Architecture: A modern engine must be "headless," meaning its logic can be accessed through a clean, well-documented Application Programming Interface (API). This allows any system - your PAS, a CRM, an agent portal, or a partner's website - to call the engine and get a rate, ensuring flexibility and seamless integration.

How It Fits into Your Tech Stack

The architectural shift from a monolithic to a decoupled approach is transformative. Instead of a single, massive core system where rating, policy, billing, and claims logic are intertwined, a modern stack separates these functions into distinct services.

In this modern architecture, the insurance rating engine is the central hub for all pricing-related matters. The Policy Administration System manages the policy lifecycle, but when it needs a price for a new business quote or an endorsement, it makes a simple API call to the rating engine. The customer-facing website does the same. This "single source of truth" model dramatically simplifies the entire IT ecosystem, making it more resilient, flexible, and easier to upgrade.

The Strategic Impact on Profitability

Ultimately, the investment in a modern insurance rating engine translates directly to the bottom line.

- Precision Pricing: Even a fractional improvement in rating accuracy across a large portfolio can lead to millions of dollars in improved loss ratios by better matching price to risk.

- Reduced Revenue Leakage: By eliminating spreadsheet errors and ensuring all approved rating factors are applied consistently, you prevent the costly revenue leakage that occurs from underpriced policies.

- Accelerated Growth: Being the first to market with an innovative product or quickly adjusting rates to capture a profitable new segment allows you to grow market share while competitors are still waiting on IT.

- Lower Operational Costs: When business users can manage rates themselves, expensive developer resources are freed up to work on true, value-added innovation instead of routine rate updates.

Conclusion

The insurance rating engine has evolved far beyond its origins as a back-office calculator. In 2025 and beyond, it is a foundational, strategic platform that dictates an insurer's agility, intelligence, and profitability. The choice for carriers is becoming increasingly clear: remain constrained by the slow, risky, and expensive rating methods of the past, or embrace the speed, accuracy, and flexibility of a modern, centralized engine. Those who make the latter choice will be best positioned to innovate, compete, and thrive in the future of insurance.

Ready To Elevate Your Insurance Software?

Connect with us today to learn more.

Subscribe to receive the latest blog posts to your inbox every week.